The Decline of Japan: Has the Country Really Yielded to China?

At the end of the 20th century, Japan seemed like a country that was about to rewrite the global economic order. Its companies were acquiring assets in the West, technologies were spreading around the world, and analysts were seriously discussing when Tokyo would surpass Washington in terms of economic scale. Today, however, the conversation more often revolves around "lost decades," demographic crisis, and stagnation. But how accurate is this picture?

In this material, we analyze statements from the video and check them for factual accuracy.

Japan as a global symbol of technological success

“In the 1980s, many spoke of Japan as an actively developing country, its economy could catch up with and even surpass the American one.”

This statement reflects not just the mood of the era, but the real structure of the world economy at the end of the 1980s. By that time, Japan had already transformed from a war-torn country into an industrial giant with a sustainable export surplus and a powerful manufacturing base.

By the end of the decade, Japan ranked second in the world in terms of nominal GDP, second only to the USA. However, what mattered more than absolute figures was the dynamics. The growth of the Japanese economy in the 1960s to 1980s outpaced most developed countries. Industrial productivity was rising, exports were expanding, and the national currency was gradually strengthening.

Particularly indicative was the composition of the largest companies in the world. In 1989, a significant portion of the global top 10 by market capitalization consisted of Japanese banks and corporations. Japan's financial institutions were considered the largest in the world by asset size. This created a sense of systemic superiority of the development model.

It is important to understand that Japan's success was not built solely on cheap production. By the 1980s, the country was already associated with quality and engineering precision. Japanese cars were perceived as reliable, home electronics as technologically advanced, and industrial equipment as highly precise. This marked a transition from the status of a "catching-up" economy to that of a standard-setting one.

Another factor was the structure of corporate governance. Keiretsu - horizontal alliances of companies around banks and industrial centers - provided stable financing and coordinated investments. This model reduced the risks of short-term shocks and allowed for the concentration of resources on long-term strategies.

Against this backdrop, there was a growing sense of loss of industrial leadership in the USA. The American press of that time regularly published articles about the "Japanese challenge." In political circles, the need for countermeasures was discussed, including currency and trade policy.

However, beneath the facade of success, structural imbalances were gradually forming. The rapid growth of assets, especially real estate and the stock market, began to detach from fundamental indicators. Corporate confidence turned into excessive optimism. The banking system actively lent against the collateral of assets whose value was constantly rising.

Thus, Japan at the end of the 1980s was indeed perceived as a potential world leader. But at the same time, it was precisely at this moment that the prerequisites for a future crisis were being laid. The paradox of the era was that the peak of confidence coincided with the accumulation of hidden risks.

And if one were to ask the question - could Japan have surpassed the USA at that time? Theoretically - yes, considering the growth rates and the scale of financial resources. Practically - this required the stability of the financial system and the ability to cool down overheating in a timely manner. The country managed this much worse than its industrial development.

The Bubble Era: Cheap Money and Overheating

“This is a wealthy country that can afford to issue loans to its citizens at the lowest possible interest rates, and mortgages for as long as 100 years.”

After the Plaza Accord of 1985, the yen sharply strengthened, which hit exporters hard. To offset this effect, the Bank of Japan lowered interest rates and expanded lending. The logic was clear - to support domestic demand.

However, cheap money began to flow not so much into production as into assets - real estate and stocks. Their prices were rising faster than the real economy. A classic bubble mechanism emerged: the increase in the value of land and stocks allowed for new loans secured by these same assets, which pushed prices even higher.

By 1989, the Nikkei index reached an all-time high, and the value of land in major cities became a symbol of financial euphoria. The banking system became deeply intertwined with the real estate market.

A 100-year mortgage is more of a journalistic exaggeration. But the overall easing of lending conditions truly reflected an atmosphere of confidence in endless growth.

The problem manifested when the regulator began to raise rates. The decline in asset prices automatically hit bank balances. This transition from credit expansion to a debt crisis became the starting point for a prolonged stagnation.

In other words, it was not just about “cheap loans,” but rather that the economy became dependent on the growth of asset prices. When that growth stopped, the system proved vulnerable.

Symbol of confidence: acquisition of Columbia Pictures

“In the same year, Sony acquires the American company Columbia Pictures.”

The fact is correct: in 1989, Sony purchased Columbia Pictures for $3.4 billion. However, the significance of this deal went far beyond business.

For decades prior, Japanese companies primarily adopted Western technologies. Now, the reverse was happening: a Japanese corporation was buying one of the iconic American film studios. It appeared as a role reversal - not a student investing in a teacher, but a fully-fledged global player acquiring a cultural asset of worldwide scale.

The deal became a symbol of the confidence of Japanese capital. In the late 1980s, Japanese investors were actively buying real estate in New York, Hawaii, and California, shares in companies, and financial assets. There was a sense that Japanese financial power was extending beyond industry and beginning to influence Western capital markets.

However, it is important to consider the context. The purchase of Columbia occurred at the peak of a financial bubble. The high value of assets within Japan created an illusion of unlimited resources. Corporations felt wealthier than fundamental indicators would suggest.

Thus, this deal simultaneously became a symbol of strength and a reflection of overheating. Just a few years after the market crash, many foreign investments turned out to be less successful than expected.

Strategy of Catching-Up Development: Licenses Instead of Inventions

“The Japanese company Toray buys a patent from Dupont and earns several times more from selling nylon worldwide.”

In the post-war decades, Japan indeed relied on a strategy of technological borrowing. Companies did not invent every technology from scratch; they purchased licenses from Western corporations, adapted the developments, and built more efficient production.

The scheme was pragmatic: acquire ready-made technology, reduce costs through labor organization and scaling, improve quality, and enter export markets.

This allowed for a rapid reduction of the technological gap without years of spending on fundamental research.

The story of licensing nylon from DuPont reflects this model. Japanese companies did not just copy the product - they optimized the production process and created competitive mass products.

It is important to understand: this was not a “copying economy.” Over time, Japan began to invest in its own R&D. But at the stage of catching up, licensing became a rational tool for accelerating modernization.

It was this combination - borrowing, improvement, and production discipline - that laid the foundation for the industrial leap of the 1960s-1980s.

Mass acquisition of patents: the scale of the phenomenon

“They purchase about 15,000 patents from various large companies…”

The exact figure requires clarification; however, the logic of the statement is correct: in the 1950s-1970s, Japan entered into thousands of licensing agreements with American and European companies. This was not about random purchases, but rather a targeted state strategy for accelerated modernization.

The Ministry of International Trade and Industry (MITI) played a key role here, coordinating technological imports and determining priority sectors. Licensing was concentrated in areas where Japan planned to achieve global leadership - chemical industry, metallurgy, machine engineering, and electronics.

It is important to emphasize: purchasing patents did not mean mechanical copying. Japanese companies, upon acquiring technology, adapted it to their own production standards, improved processes, and reduced costs. Often, it was organizational innovations - quality control, lean manufacturing, optimization of supply chains - that provided an advantage, rather than the original technology itself.

Thus, the scale of licensing reflected not dependence, but strategic calculation. It was a way to quickly integrate into the global technological system, reducing the gap in one or two decades instead of several generations.

That is why by the 1980s, Japan had already ceased to be merely a “buyer of technology” and had itself become a source of innovation in several industries.

The Japanese challenge to the American automotive industry

“In the 1970s, American cars sell best in America… After some time, Toyota breaks through to the leaders…”

Until the 1970s, the American automotive market was effectively controlled by domestic manufacturers - Ford, General Motors, Chrysler. Their models were large, powerful, and focused on cheap fuel.

The situation changed after the oil crisis of 1973. The sharp rise in gasoline prices forced consumers to reconsider their preferences. Economical, compact, and reliable cars became a priority. And it was here that Japanese manufacturers were strategically prepared.

Toyota, Honda, and Nissan were already producing small cars with low fuel consumption. But it wasn’t just about the size of the vehicle. Japanese companies built a different manufacturing philosophy - stricter quality control, process optimization, and reduced defects. This allowed them to maintain prices while ensuring high reliability.

As a result, by the end of the 1970s, Japanese cars began to actively capture the American market. Their share was growing, and along with it, the pressure on local manufacturers. For the U.S., this became not just a trade issue, but a structural challenge to the industrial model.

Electronics as a Global Standard

A similar process occurred in the electronics sector. Panasonic, Sony, Toshiba, and other companies gradually built a reputation as manufacturers of reliable and technologically advanced products. By the 1980s, Japanese electronics were perceived not as an alternative to Western products, but as a benchmark for quality.

It is important to note that success was not built solely on low prices. Japanese companies focused on mass production while maintaining precision. Quality control, process standardization, and continuous improvement (kaizen) allowed them to minimize defects and reduce costs without sacrificing reliability.

Moreover, Japan actively developed the production of components - chips, displays, memory storage. This meant not just assembling finished devices, but having control over key technological links. In the 1980s, Japanese manufacturers held a significant share of the global semiconductor memory market.

Electronics became a kind of showcase for the Japanese industrial model. It combined licensed technology, production discipline, and scaling. As a result, Western companies began to lose ground in the consumer segment.

The success of Japanese electronics was not a result of dumping, but rather a consequence of systemic competitiveness. This heightened tensions in trade relations with the USA and became one of the factors that led to the currency coordination of the mid-1980s.

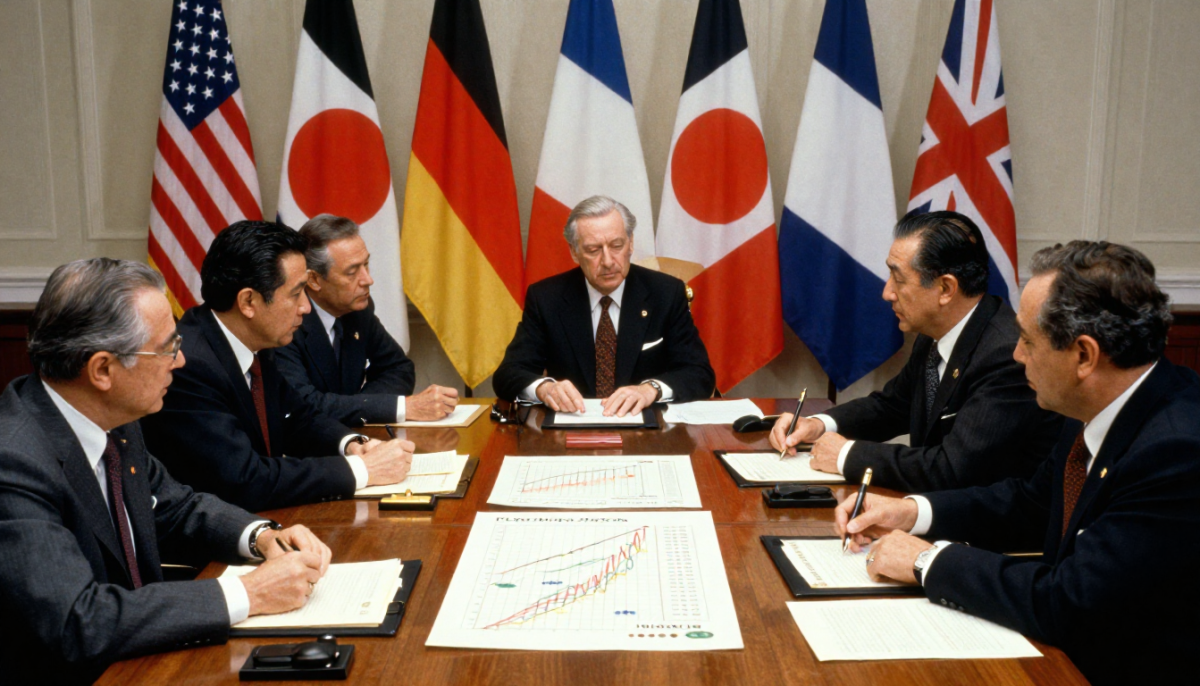

Plaza Accord: A Turning Point

“In September 1985, countries such as the USA, Germany, France, the UK, and Japan agreed to align their currency exchange rates.”

This refers to the Plaza Accord, signed in September 1985 by the finance ministers and central bank governors of the five largest economies. Its main goal was to weaken the excessively strong US dollar.

By the mid-1980s, the dollar had strengthened significantly, making American exports less competitive and exacerbating the US trade deficit—primarily in relations with Japan. Political pressure within the US was growing, and a systemic solution was required.

The agreement provided for coordinated currency interventions. The result was swift and substantial: within two years, the dollar weakened noticeably, while the yen strengthened significantly—almost doubling in value against the American currency.

For the US, this meant improved competitive positions for exports. For Japan, it posed a serious challenge. The export-oriented economy suddenly faced rising prices for its goods abroad. Company profits were shrinking, and growth rates came under pressure.

It is important to emphasize: the Plaza Accord itself did not "crash" the Japanese economy. However, it marked the point after which the growth model based on a weak currency and export expansion ceased to function as before. Japanese authorities attempted to compensate for this shock with domestic stimulus—and it was this reaction that subsequently contributed to the formation of a financial bubble.

Interpretation error: trading did not stop

“In 1985, all trade relations with Japan were terminated.”

This statement is not accurate. Neither in 1985 nor after the signing of the Plaza Accord did trade between the USA and Japan cease. The discussion was about coordinating monetary policy, not about breaking economic ties.

Moreover, the volume of bilateral trade continued to be significant. The issue was not the absence of trade but its structure. The USA experienced a persistent trade deficit with Japan, which created political pressure domestically. American manufacturers accused Japanese companies of unfair competition, and lawmakers discussed the possibility of introducing protectionist measures.

It was in this context that the Plaza Accord became a compromise solution. Instead of sharply raising tariffs and starting a full-scale trade war, the parties chose currency adjustment as a tool for restoring balance.

It is important to understand the difference: terminating trade would mean an economic rupture. Currency coordination is an attempt to change the terms of trade without destroying the exchange system itself.

The Burst Bubble and the Beginning of the "Lost Decade"

By 1989, real estate and stock prices in Japan had reached historic highs. The Nikkei stock index approached the mark of 39,000 points - a level that would not be regained for decades. The value of land in major cities had detached from economic realities.

The turning point came in the early 1990s when the Bank of Japan began tightening monetary policy. The increase in interest rates sharply cooled the market. Asset prices began to decline - first gradually, then accelerating. The bubble started to deflate.

The key problem lay in the structure of the financial system. Banks actively lent against real estate and stocks. When the value of these assets fell, the collateral depreciated, and loans turned into non-performing ones. Huge volumes of bad debts accumulated on the banks' balance sheets.

Instead of a quick cleansing of the system, a prolonged restructuring process began. Banks were slow to recognize losses, companies postponed write-offs, and the government avoided drastic reforms. This allowed for the avoidance of an immediate collapse but stretched the crisis over years.

The economy entered a period of low growth, deflationary pressure, and investment caution. This stage was later referred to as the "lost decade" - although in reality, stagnation lasted longer.

The decisive factor was not the mere fact of the market's decline, but the system's inability to quickly redistribute resources and restore momentum. The financial crisis transformed into a structural stagnation.

Zombie companies: support instead of reforms

“These are the companies that received the name ‘zombie’…”

The term “zombie companies” is indeed used in economic literature. It refers to enterprises that formally continue to operate but are unable to service their debts from their own profits and survive thanks to constant support from banks or the government.

After the bubble burst, the Japanese banking system became overloaded with problematic loans. Mass bankruptcies would have meant a sharp deterioration in bank balances and a surge in unemployment. Therefore, many financial institutions preferred to extend loans to weak borrowers instead of recognizing losses.

From a short-term perspective, this seemed rational. The economy avoided shock therapy, employment was preserved, and there was no sharp social crisis. However, in the long term, such a strategy had costs.

Capital and labor continued to remain in low-efficiency companies. Resources were not redistributed to more productive sectors. Competition and innovative dynamics weakened. Productivity grew slowly, and investment activity remained restrained.

This effect - the slowdown of the economy's “cleansing” - became one of the factors of prolonged stagnation. Instead of a sharp but short crisis, Japan experienced a long period of low growth and caution.

Thus, the problem lay not only in the bubble itself but also in how the system reacted to its collapse. Support instead of structural reform allowed the situation to stabilize but simultaneously entrenched economic inertia.

Why haven't new global giants emerged?

“Can you recall… a new breakthrough Japanese company?”

This question sounds like a reproach, but it is more accurate to consider it through the lens of structural changes in the global economy. In the 1990s and 2000s, the center of technological growth shifted from industrial production to digital platforms and software ecosystems.

American IT companies emerged as leaders, building businesses around software, the internet, and network effects. Later, Chinese platforms scaled a similar model. Their advantage lay not only in technology but also in their ability to quickly capture global markets through the scalability of digital products.

Japan, on the other hand, maintained strong positions in traditionally industrial sectors—automotive, robotics, manufacturing equipment, and components. These are capital-intensive and engineering-complex industries, but they do not create the same global network ecosystems as digital platforms.

Moreover, the Japanese corporate model focused on stability and long-term relationships rather than aggressive venture growth. The startup culture developed more slowly, and the capital market was less inclined to take risks.

As a result, Japan did not lose its technological competence but became less represented in the new digital architecture of the global economy. This created a sense of the absence of “new giants,” although Japanese companies still play a key role in several high-tech niches.

So, the question is not so much about the lack of innovations as it is about the changing type of innovations that have come to define global leadership.

Demography as a Structural Challenge

“Every third person in the country is over 65 years old.”

Aging population is not a journalistic exaggeration, but a persistent demographic trend. Japan indeed ranks among the countries with the highest proportion of elderly people in the world. This is not a short-term phenomenon, but a result of a long-term decline in birth rates and high life expectancy.

Since the 1980s, the birth rate in the country has consistently remained below the level of simple reproduction. At the same time, the average life expectancy is one of the highest in the world. As a result, the age structure is gradually shifting upwards.

The economic consequences are multilayered.

Firstly, the working-age population is decreasing. This means a smaller influx of young workers, reduced potential growth rates, and increased competition for labor.

Secondly, the burden on the pension and healthcare system is increasing. With fewer employed individuals, the share of social benefit recipients grows. This requires either an increase in the tax burden or an increase in public debt.

Thirdly, the structure of consumption is changing. An aging society is less oriented towards risk and innovation, which indirectly affects entrepreneurial activity and investment decisions.

Japan is trying to adapt: automation, robotization, extending the working activity of the elderly, cautious migration policy. However, demographics is a factor that is difficult to adjust quickly.

Aging population is not a consequence of economic decline, but it exacerbates its effects. In the context of already existing stagnation, the demographic shift becomes an additional constraint for accelerated growth.

Karoshi and work culture

“There is a term – karoshi…”

The term “karoshi” – death from overwork – is indeed officially used in Japan and recognized at the state level. It emerged in the 1970s when cases of sudden death among workers due to extreme overtime and chronic stress began to be recorded.

However, it is important to separate the symbol from the statistical norm. Extreme overtime is not a universal daily reality for every worker. Nevertheless, the issue of labor overload is acknowledged by the state, and cases of karoshi are investigated and can serve as grounds for compensation to families.

The roots of the phenomenon lie in the corporate culture of the post-war period. The Japanese employment model was long built on principles of lifetime employment, high company loyalty, and collective responsibility. The workplace was perceived not just as a source of income but as part of social identity.

In times of economic boom, such a culture reinforced production discipline and contributed to growth. But during periods of stagnation, it began to create additional pressure. The reduction in the number of workers due to demographics increased the burden on those remaining, while corporate inertia made it difficult to transition to more flexible employment formats.

In recent years, the government has taken steps to limit overtime and reform labor legislation. Nevertheless, the issue of balancing production efficiency and quality of life remains sensitive.

Thus, karoshi is not a mass norm but an extreme manifestation of a broader problem of labor culture, shaped in an era of rapid growth and found to be less adaptable to a prolonged period of stagnation.

The Chinese path: repetition or alternative?

“China started exactly the same way…”

At first glance, the similarities are indeed obvious. Both Japan in the post-war period and China at the end of the 20th century focused on export-oriented production, integration into global trade, and technological borrowing. Both countries employed a strategy of gradually complicating their industrial structure - from simple goods to more technologically advanced products.

However, upon closer examination, the differences turn out to be fundamental.

Firstly, monetary policy. China has maintained stricter control over the yuan's exchange rate and financial flows. The state actively manages capital movement and prevents sharp currency fluctuations comparable to what happened with the yen after the Plaza Accord. This reduces the likelihood of a sudden currency shock.

Secondly, the scale of the domestic market. China has a significantly larger demographic base, which allows it to compensate for external constraints with domestic demand. Japan in the 1980s remained more dependent on exports.

Thirdly, the financial architecture. The Chinese banking system is closely linked to the state and is used as a tool of industrial policy. This creates different risks but simultaneously allows for quicker coordination of investment flows.

Finally, the stage of global integration differs in historical context. Japan developed under the dominance of the United States and a relatively stable financial system. China operates in a world of existing globalization, digital platforms, and trade conflicts.

Therefore, directly equating the trajectories simplifies the picture. There is a similarity at the level of the catching-up growth model, but the institutional environment, the scale of the economy, and the tools of state control differ.

The question is not whether “China will repeat Japan's fate,” but which structural risks - asset overheating, debt burden, demographics - will prove critical for it. Japan's history serves more as a warning about potential consequences than as an accurate blueprint for the future.

Sources

- World Economic Outlook - International Monetary Fund - 2023

- Historical Statistics - World Bank

- Plaza Agreement - U.S. Department of the Treasury - 1985

- Asset Price Bubble and Monetary Policy - Bank of Japan

- The Walking Dead? Zombie Firms and Productivity - Bank for International Settlements - 2018

- OECD Economic Surveys: Japan - OECD - 2021

- Population Statistics of Japan - Statistics Bureau of Japan - 2022

You might like

Will China surpass America? What lies behind the growth and global ambitions?

The question of whether China will overtake the United States in economic power is now being discussed not only in academic circles but also in everyday conversations...

This is why the history of LEGO is more complex than it seems.

The history of LEGO is often presented as an almost flawless entrepreneurial legend: a master from a provincial Danish town, a crisis, a bold decision to re...

Elon Musk - Genius or Calculating Entrepreneur? What Really Lies Behind His Story

The story of Elon Musk has long turned into a modern entrepreneurial legend. He is called a visionary, an adventurer, a genius, a disruptor of industries...

China on the path to global leadership: how sustainable is this growth?

China has undergone a transformation in recent decades that took centuries in other countries. From an agrarian, poor nation torn by internal conflicts...